In a significant move to protect policyholders, the Reserve Bank of India (RBI) Governor, Sanjay Malhotra, has issued a stern warning against the rampant mis-selling of financial products. During the post-MPC (Monetary Policy Committee) press conference in February 2026, the Governor emphasized that banks and insurance companies would be held strictly accountable for unethical sales practices.At Bimacure, we welcome this proactive stance by the regulator. As a leader in insurance grievance redressal, we have seen thousands of families struggle with "forced bundling" and "hidden terms." This new directive provides a much-needed legal shield for consumers.What is Mis-selling? (And Why It’s Now an Offence)In banking and insurance, mis-selling occurs when a product is sold without full disclosure or is completely unsuitable for the customer’s needs. Under the new 2026 RBI guidelines, mis-selling is now categorized as a serious violation of Responsible Business Conduct.Most Searched Signs of Mis-selling in 2026: Forced Bundling: Being told that a "Home Loan" or "Personal Loan" is only possible if you buy a life insurance policy. The "FD" Trap: Agents selling traditional endowment plans by falsely claiming they are "Fixed Deposits" with higher returns. Hidden Fees & Charges: Not disclosing the high surrender charges or premium allocation charges in ULIPs. Suitability Violations: Selling long-term, high-premium policies to senior citizens who need liquidity. RBI’s New "Zero-Tolerance" FrameworkThe Governor’s warning isn't just verbal; it is backed by the Draft Directions for Responsible Business Conduct (2026). These rules, set to be fully enforced by July 2026, include: Full Refunds: If mis-selling is proven, the bank must refund the entire premium amount plus compensation for losses. Ban on Third-Party Incentives: To curb aggressive sales, banks are prohibited from giving direct incentives to employees for pushing insurance or mutual fund products. Mandatory Post-Sale Feedback: Banks must seek customer feedback within 30 days to ensure the product features were understood. The Impact: Security for the Common ManThe human cost of mis-selling is immense. Many retirees have seen their life savings locked into "Worthless Policies" that mature when they are 85. The RBI's stricter stance, combined with IRDAI’s Bima Bharosa portal, aims to reduce these malpractices and restore trust in the financial ecosystem.How Bimacure Helps Victims of Mis-sellingAt Bimacure Insure Sol, we specialize in helping victims navigate the complexities of insurance claim disputes and mis-selling cases. If you have been misled by an agent or a bank manager, we provide: Expert Case Analysis: We identify the exact regulatory violations in your policy. Evidence Building: We help you document "Dark Patterns" or "Forced Consent" to build a strong case. End-to-End Resolution: From filing complaints with the Insurance Ombudsman to representing you at the Bima Lokpal, we fight for your 100% refund. Don't Suffer in Silence. If you have been a victim of unethical financial practices, contact Bimacure today. We are committed to securing justice and reclaiming your hard-earned money. Source Credit: Financial Express. Original Article: Mis-Selling of Products to be Taken Very Seriously: RBI Guv Cautions Banks.

Continue Reading

Insurance serves as a safety net, offering financial protection during unforeseen events. However, for many policyholders in India, the journey from filing a claim to receiving the settlement is fraught with challenges. Mis-selling of policies and delayed claim settlements have become pressing concerns, leaving many in distress.Understanding Mis-Selling in InsuranceMis-selling refers to the unethical practice where insurance policies are sold to customers without proper disclosure of terms, or by providing misleading information. This often results in policyholders purchasing products that don't align with their needs or financial capabilities.Real-Life Incidents Highlighting the Issue1. Case of Elderly Individuals Mis-Sold PoliciesIn several Tier II and III cities, there have been instances where individuals aged above 75 were sold life insurance policies. Often, these senior citizens were not made aware of the policy terms, leading to financial strain and dissatisfaction. Such practices have raised concerns about the ethical standards of certain financial institutions.2. Housing Loan Borrowers Coerced into Buying InsuranceThe National Housing Bank (NHB) reprimanded housing finance companies for bundling insurance policies with home loans without adequately informing borrowers. Many borrowers found themselves paying for insurance policies they neither needed nor understood, adding to their financial burdens. Challenges in Claim SettlementsEven after purchasing policies, policyholders often face hurdles during claim settlements:High Rate of Claim RejectionsIn the financial year 2023-24, Star Health and Allied Insurance Co. Ltd. recorded the lowest claim settlement ratio within three months among all stand-alone health insurers, settling only 82.31% of claims in that period. Such statistics highlight the challenges policyholders face in receiving timely claim settlements.Delayed Settlements Leading to Financial StrainA survey revealed that 43% of health insurance policyholders who submitted claims in the past three years faced issues in receiving their money or settling hospital bills after treatment. Delays in claim rejection settlements can lead to significant financial and emotional distress for families already grappling with medical emergencies.Steps to Address Mis-Selling and Claim Settlement Issues1. Stay InformedBefore purchasing any insurance policy, thoroughly research and understand the product. Ensure it aligns with your financial goals and needs.2. Utilize the Free-Look PeriodThe Insurance Regulatory and Development Authority of India (IRDAI) mandates a free-look period (typically 15-30 days) during which policyholders can cancel their policy without penalties if they find discrepancies or are unsatisfied with the terms.3. Report Mis-SellingIf you believe you've been mis-sold a policy, report it to the insurance company immediately. If unresolved, escalate the matter to IRDAI or consumer forums.4. Seek Legal RecourseIn cases of unjust claim rejections or delays, consider approaching consumer courts or seeking legal counsel to address the grievance.ConclusionWhile insurance is essential for financial security, it's crucial for policyholders to remain vigilant and informed. By understanding the nuances of insurance products and being aware of one's rights, individuals can better navigate the complexities of claim settlements and protect themselves from potential pitfalls.

Continue Reading

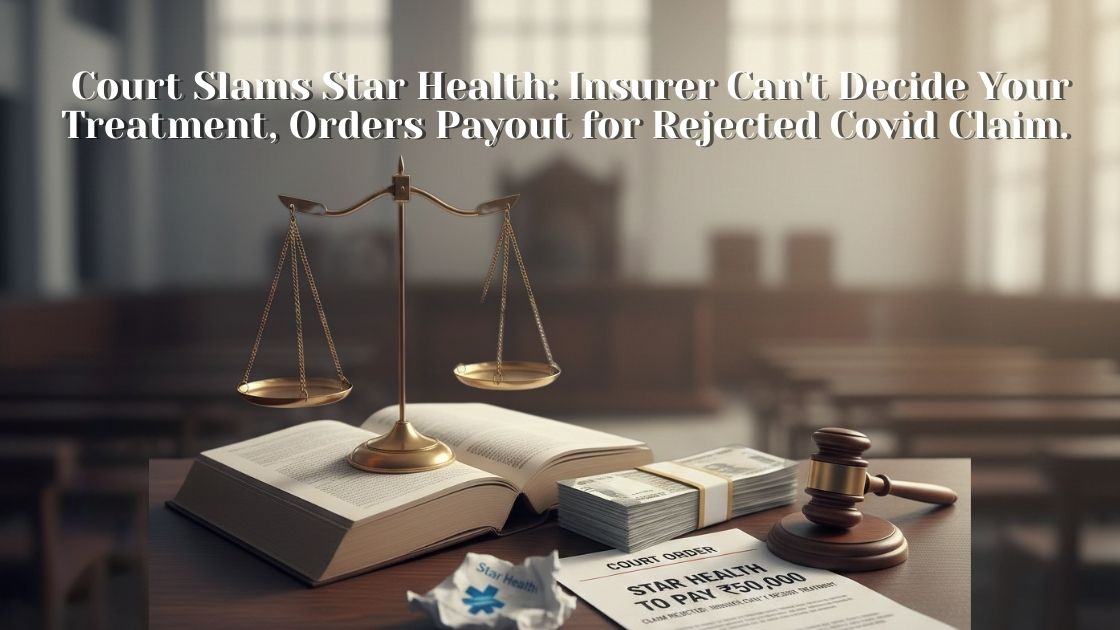

The Insurance Regulatory and Development Authority of India (IRDAI) has placed Star Health and Allied Insurance under scrutiny due to concerns regarding their claim settlement practices. Policyholders have raised multiple complaints, alleging unfair treatment and delays in claim processing. This development has once again highlighted the ongoing issues in the insurance sector, where customers often find themselves struggling to receive the benefits promised by their policies.The Issue at HandStar Health Insurance, one of India's leading standalone health insurers, has been flagged for its handling of claim settlements. Reports suggest that numerous policyholders have faced unexpected denials, excessive delays, and non-transparent claim processing methods. Given the critical nature of health insurance, such practices put immense financial and emotional stress on individuals who rely on their insurance for medical emergencies.IRDAI's InterventionWith an increasing number of grievances being reported, IRDAI has stepped in to investigate and ensure that Star Health is complying with fair claim settlement procedures. The regulatory body has been closely monitoring insurers across India to ensure that companies adhere to ethical and legal standards in their claim processes.Bimacure’s Role in Helping VictimsFor policyholders who have been affected by unfair insurance claim rejections or delays, Bimacure provides a platform to fight against such injustices. As a company specializing in claim recovery and financial dispute resolution, Bimacure helps customers navigate the complex world of insurance claims. By offering expert assistance, guiding customers on documentation, and engaging in negotiations with insurance companies, Bimacure ensures that policyholders receive what they rightfully deserve.What Can Policyholders Do?If you have experienced issues with your health insurance claims, you can take the following steps:File a Complaint with IRDAI: Use the IRDAI grievance redressal system to officially report any claim-related problems.Seek Legal Advice: If your claim has been wrongfully denied, you can explore legal options for redressal.Contact Bimacure for Assistance: Our team at Bimacure can help you recover your rightful claim, ensuring that insurance companies adhere to the guidelines set by IRDAI.ConclusionThe scrutiny of Star Health’s claim settlement practices is a reminder that policyholders need to be vigilant and proactive in securing their rights. With IRDAI stepping in to regulate the situation, there is hope for a more transparent and customer-friendly insurance sector. Meanwhile, organizations like Bimacure continue to work towards protecting individuals from insurance-related injustices.Disclaimer: This blog is for informational purposes only. All rights of the original article belong to the respective.

Continue Reading

The issue of mis-selling insurance products by housing finance companies has once again come under the spotlight. Regulatory authorities have pulled up multiple housing financiers for aggressively bundling life and general insurance policies with home loans, often without proper consent from customers. This malpractice continues to plague the sector, raising serious concerns about consumer protection and transparency in financial dealings. Unethical Insurance Practices in Housing Finance Several housing finance companies have been found compelling borrowers to purchase insurance policies as a pre-condition for loan approvals. In many cases, customers are unaware of these additional charges, which significantly inflate their loan costs. Reports indicate that lenders often misrepresent insurance policies, portraying them as mandatory when, in reality, borrowers have the right to choose their insurers. Regulators, including the Reserve Bank of India (RBI) and the Insurance Regulatory and Development Authority of India (IRDAI), have taken note of these unethical practices. Consumer complaints regarding forced insurance bundling have surged, prompting authorities to issue fresh warnings to housing finance firms. The crackdown is aimed at ensuring fair practices and protecting home loan borrowers from undue financial burdens.How Bimacure Helps Victims of Mis-Selling Bimacure, powered by Insucure Solutions India (OPC) Pvt. Ltd., actively assists individuals who have been victims of such fraudulent practices. Many home loan borrowers approach Bimacure seeking help in recovering their hard-earned money from wrongly sold insurance policies. Our team of experts thoroughly examines each case, guiding customers through the complaint and refund process. Through strategic intervention, Bimacure has successfully helped numerous clients reclaim their money from financial institutions engaging in mis-selling of insurance policy. Our approach includes filing grievances with regulatory bodies, raising legal complaints, and negotiating with financial companies to ensure justice for our clients.Consumer Rights and Awareness Consumers must stay vigilant and aware of their rights when applying for loans. Here are a few essential points to remember:Insurance is not mandatory: Lenders cannot force borrowers to purchase insurance from a particular provider.Seek clarity on charges: Always demand a detailed breakup of loan-related costs before signing any agreement.Report mis-selling: If you feel pressured or misled into buying an insurance policy, immediately report it to IRDAI or RBI.Consult experts: Organizations like Bimacure can provide guidance and support in challenging wrongful financial transactions.Final Thoughts While regulators are tightening their grip on housing financiers indulging in mis-selling, consumers must also exercise due diligence to protect themselves from financial exploitation. If you or someone you know has been a victim of insurance mis-selling, Bimacure is here to help you fight back and reclaim what is rightfully yours.Disclaimer: This blog is based on an original article published by The Economic Times. All rights to the original content are reserved by the respective publisher.

Continue Reading

Filing insurance claims can be a complicated and stressful process, especially when you’re dealing with the emotional and financial burden of a loss. Whether it’s an auto accident, property damage, or a health issue, filing insurance claims correctly is crucial for a smooth and quick settlement. Unfortunately, many people make common mistakes that can delay or even deny their claims.In this article, we’ll guide you through the key pitfalls to avoid and share a real-world incident that highlights why it’s so important to handle your claims carefully.1. Delaying the ClaimOne of the most common mistakes when filing insurance claims is waiting too long to notify your insurer. Most insurance policies have strict timelines for reporting incidents. Delaying can make the claim process harder or lead to a denial.Tip: Report any incidents immediately, even if you’re still gathering all the necessary documents. Early notification shows you acted in good faith.2. Not Understanding Your PolicyMany claimants don’t take the time to thoroughly understand what their policy covers. This can lead to wrong expectations and mistakes during the claim process.Tip: Review your insurance policy in detail before filing a claim. If anything is unclear, ask your insurer or broker for clarification.3. Failing to Document EverythingProper documentation is critical. Failing to take pictures, collect reports, or keep receipts can weaken your claim.Tip: After an incident, take photographs, gather police or medical reports, and maintain a record of all communications with your insurer.4. Making Inaccurate StatementsEven minor inaccuracies can severely damage your case. Insurers can deny claims if they find discrepancies between your statements and the evidence.Tip: Be honest and detailed. If you’re unsure about something, say so rather than guessing.5. Accepting the First Settlement OfferInsurance companies often try to settle claims quickly and may offer a lower amount initially. Many people accept the first offer without negotiation, losing out on fair compensation.Tip: Review any settlement offer carefully and don’t hesitate to negotiate or seek legal advice if needed.Real-Life Incident: Lessons from the 2021 Texas Winter Storm ClaimsA vivid example of filing insurance claims gone wrong comes from the devastating Texas winter storm in February 2021.According to a report from The Texas Tribune, thousands of homeowners filed claims for water damage and broken pipes. However, many claims were delayed or denied because homeowners didn’t properly document the initial damages or waited too long to file. Some even made unauthorized repairs before contacting their insurers, which made it difficult to prove the extent of the original damage.(Source: The Texas Tribune)This incident highlights how crucial it is to file insurance claims promptly, document everything, and follow insurer guidelines closely.ConclusionFiling insurance claims doesn't have to be a nightmare. By avoiding these common mistakes, you can improve your chances of a successful, hassle-free claim. Always stay organized, be honest, act quickly, and understand your policy well.If you find the process overwhelming, don't hesitate to seek professional help. A little diligence today can save you a lot of trouble tomorrow.

Continue Reading

An insurance plan plays a crucial role in safeguarding you and your family against life’s uncertainties. Among these, term insurance stands out as a pure life insurance policy that provides financial protection to your beneficiaries if you pass away during the policy term. Unlike other plans, it does not offer any savings or investment returns.Insurance expert Nikhil Jha recently emphasized on social media that term insurance is the only life insurance worth buying. He explained that term insurance is straightforward protection - no returns, no gimmicks, just reliable financial security for your loved ones if something happens to you.“Life Insurance Gyan: Term life insurance is the only life insurance to buy. Don’t be fooled by LIC or other insurers pushing policies with guaranteed returns after many years. Mis-selling is the biggest scam in life insurance,” Jha wrote on X.He pointed out that many people get trapped into buying expensive endowment plans, money-back policies, or guaranteed return schemes aggressively marketed by LIC and other agents. These policies promise maturity payouts after 20 to 30 years but often come with poor returns (around 4–5%), high commissions, and long lock-in periods that aren’t clearly disclosed.Term insurance in today’s contextTerm insurance offers a cost-effective way to ensure your family is financially protected if you die during the policy term. Compared to life insurance plans that combine maturity and death benefits, term plans have lower premiums. They can also be tailored to fit your specific needs.In contrast, whole life insurance plans provide lifelong coverage along with investment benefits. These plans often cover up to age 100 and allow cash accumulation over time. Policyholders can also add riders like critical illness coverage for extra protection against medical emergencies.While life insurance plans can help accumulate wealth through savings or investments, term insurance focuses solely on providing financial security for a fixed period at an affordable price. Both require premium payments, which guarantee the benefits outlined in the policy.Life insurance plan vs. term insurance planA life insurance plan offers financial security for your family if you pass away and also includes a cash accumulation feature to support future financial goals. Policy terms can range from 5 to 30 years or even cover a lifetime. If you die during the term, your beneficiaries receive a lump sum death benefit to cover expenses like debts, children’s education, medical bills, or daily costs.Term insurance, however, covers you only for a specific period but usually provides higher coverage amounts at lower premiums.Premium comparison: life insurance vs. term insuranceBuying insurance early in life usually means lower premiums. Some insurers provide coverage for partial or permanent disability affecting your income during the policy term.The key difference is that term insurance does not pay any maturity benefit if you survive the policy term, which keeps premiums lower. Despite this, term plans guarantee a minimum sum assured payment if the insured event occurs during the term, making them affordable yet comprehensive.Both term and life insurance protect your family financially in case of premature death. Life insurance plans often include a survival benefit, paying a lump sum if you outlive the policy term, which can serve as a retirement fund or financial safety net.In summary, term insurance is the most straightforward and cost-effective way to secure your family’s financial future, while other life insurance plans mix protection with investment but often at a higher cost and with lower returns. Avoid falling for mis-sold policies promising guaranteed returns and focus on pure protection through term insurance.Experts ApproachBimacure, as an expert insurance consultant, is committed to helping policyholders efficiently address and resolve their insurance grievances. They focus on ensuring fair claim settlements and combating mis-selling practices to protect the interests of both customers and insurers. By providing expert guidance and support throughout the complaint process, Bimacure helps policyholders navigate complex insurance issues and secure the compensation they deserve. Their dedication makes them a reliable partner for resolving insurance disputes effectively and transparently.

Continue Reading

The life insurance sector kicked off FY26 with a mixed bag of performances in April 2024. While private players like Axis Max Life and HDFC Life showcased robust growth across key segments, the state-owned Life Insurance Corporation of India (LIC) continued to face headwinds in its retail premium business. Let’s dive into the numbers and decode what April’s data reveals about India’s evolving insurance landscape. ---HDFC Life: Steady Demand Amid Competitive Pressures- Total Premiums: +23% YoY - APE (Annual Premium Equivalent):+10% YoY - Retail APE: +3% YoY HDFC Life started FY26 on a stable note, with total premiums surging 23% year-on-year. While retail APE growth remained modest at 3%, the steady uptick in APE (10%) signals sustained demand for its product portfolio. The insurer’s focus on diversified offerings and digital outreach appears to be paying off in a competitive market. ---ICICI Prudential: Retail Drags Growth- Total Premiums: +10% YoY - APE: +5% YoY - Retail APE: -16% YoY ICICI Prudential faced challenges in its retail segment, with retail APE declining 16% YoY despite a 10% rise in total premiums. This slump highlights potential gaps in customer acquisition or product alignment in a segment that’s critical for long-term profitability. However, the insurer’s group business may have offset some of this weakness, keeping overall APE growth positive. ---Axis Max Life: The Star Performer- Total Premiums: +17% YoY -APE: +23% YoY - Retail APE:+24% YoY Axis Max Life emerged as the standout player in April, with retail APE soaring 24% YoY—the highest among peers. Its balanced growth across total premiums (17%) and APE (23%) underscores effective distribution strategies and strong customer retention. The insurer’s agility in adapting to market trends, such as tech-driven policy management and tailored products, likely fueled this momentum. ---SBI Life: Stability Over Speed - Total Premiums: +0.3% YoY - APE: +8% YoY - Retail APE: +2% YoY SBI Life’s muted 0.3% premium growth suggests a cautious start to FY26. However, the 8% rise in APE and marginal retail APE growth (2%) indicate a focus on quality over quantity. As one of India’s largest insurers, SBI Life’s emphasis on sustainable growth and risk management could position it well for long-term stability. ---LIC: Retail Struggles Persist - Total Premiums: +10% YoY - APE: -1% YoY - Retail APE: -4% YoY LIC’s retail APE fell 4% YoY in April, even as total premiums grew 10%. This underperformance reflects ongoing challenges in competing with private insurers’ digital-first models and personalized customer engagement. While LIC’s massive agent network and brand legacy drive bulk premiums, its retail segment—a key profitability driver—needs urgent innovation to regain lost ground. ---The Big Picture: Private Players Outpace LIC April’s data underscores a clear divide: private insurers are leveraging agility, tech adoption, and customer-centric products to dominate retail growth, while LIC struggles to translate its scale into retail success. Axis Max Life’s stellar performance and HDFC Life’s resilience highlight the importance of innovation in a sector where consumer preferences are rapidly evolving. For LIC, the road ahead involves revitalizing its retail strategy—possibly through digital transformation, niche products, or partnerships—to bridge the gap with private rivals. Meanwhile, private insurers must sustain their momentum by doubling down on customer experience and expanding reach in underserved markets. ---Why This Matters for Policyholders and Investors- The shifting dynamics in India’s life insurance sector reflect broader trends: customers increasingly prioritize flexibility, transparency, and digital convenience. For investors, private insurers’ consistent retail APE growth signals strong fundamentals and long-term value. For policyholders, competition is driving better products and services—a win-win for all stakeholders. At *Bimacure*, we believe in decoding industry trends to empower businesses and consumers with actionable insights. Stay tuned as we track FY26’s evolving insurance landscape and what it means for you! --- [Bimacure] – Your Partner in Navigating Financial Trends (Note: Data sourced from April 2024 regulatory filings and industry reports.)

Continue Reading

Introduction: Insurance mis-selling in India has become a significant concern, affecting countless policyholders. Mis-selling occurs when insurance products are sold by providing misleading information or without adequately explaining the terms, leading to unsuitable policies for the buyers. Common Forms of Mis-Selling: Inadequate Disclosure: Agents often fail to disclose critical policy details, such as exclusions or waiting periods. Pressure Tactics: Customers are sometimes coerced into buying policies they don't need. Misrepresentation: Policies are presented as investment tools with guaranteed returns, which may not be accurate. Impact on Consumers: Mis-sold policies can lead to financial losses, lack of coverage when needed, and a general mistrust in the insurance sector. Conclusion: Awareness and understanding of insurance products are crucial. Consumers should thoroughly read policy documents and seek clarification on any doubts before purchasing. Disclaimer: Bimacure does not hold any rights to this blog. All rights reserved by the original blog resources.

Continue Reading

Case Study 1: A 70-year-old NRI woman was reportedly lured into purchasing an insurance plan under the pretext of mandatory requirements while opening an NRE account, leading to a significant financial commitment she was unaware of . Case Study 2: In a massive Rs 500 crore insurance scam, fraudulent life and vehicle policies were issued across 12 states, involving fake documentation and even orchestrated murders to claim insurance payouts . Conclusion: These cases highlight the severe consequences of insurance mis-selling and the importance of vigilance and due diligence by consumers. Disclaimer: Bimacure does not hold any rights to this blog. All rights reserved by the original blog resources.

Continue Reading

Filing an insurance claim can feel daunting—especially when you’re already dealing with a medical emergency, property loss, or personal distress. But understanding how the insurance claims settlement process works can reduce anxiety and help you claim what’s rightfully yours.This guide breaks down the four essential stages of the insurance claims settlement process in India—whether you're dealing with health, motor, or life insurance.What Is Insurance Claims Settlement?The insurance claims settlement process is the procedure through which an insurance company assesses, verifies, and pays out a claim made by the policyholder or nominee. In India, this process is governed by the Insurance Regulatory and Development Authority of India (IRDAI), which ensures transparency, fairness, and timely settlement.Stage 1: Intimation of the ClaimThe first and most crucial step is notifying the insurer about the event as soon as possible. This is called claim intimation.What You Need to Do:Inform the insurer via their toll-free number, website, mobile app, or email Provide policy details, date/time of the event, and brief descriptionFor health insurance: inform within 24-48 hours (for hospitalisation)For motor or life insurance: ideally within 7 days (or as specified in the policy)Why It Matters:Delays in intimation can result in claim rejection, especially if it violates policy terms.Stage 2: Documentation and VerificationOnce the claim is raised, the insurer will request supporting documents based on the type of policy.Common Documents Required:Policy copyClaim form (duly filled)Hospital bills/discharge summary (for health insurance) FIR and repair bills (for motor insurance)Death certificate and KYC (for life insurance)The insurer then verifies the documents and may initiate an investigation if needed.Tip:Always keep original documents and scan digital copies. Ensure names and dates match across all paperwork to avoid delays.Stage 3: Assessment and ApprovalOnce the documentation is verified, the insurer assesses the validity of the claim. What Happens:The claim is examined against the terms and conditions of the policyFor cashless claims (like health insurance), the hospital and insurer coordinate directlyFor reimbursement claims, the insurer reviews bills and determines payable amounts In life insurance, nominee details and cause of death are examined carefullyIf everything is in order, the claim is approved. If discrepancies are found, it may be queried or denied.Stage 4: Settlement and PayoutThe final stage is the actual settlement of the claim. Once approved, the payout is processed.Payout Modes:NEFT transfer to the policyholder or nominee’s bank account Direct payment to hospitals (in cashless cases)Cheques in some legacy or rural casesTimelines as per IRDAI:Claims must be settled within 30 days of receiving all required documentsIf an investigation is initiated, it must be completed within 90 days, with payment made within 30 days thereafterCommon Issues Faced During Insurance Claims SettlementClaim rejection due to non-disclosure of pre-existing conditions Delay in filing or incomplete documentationDisagreements over claim amount or repair costs Lack of clarity on policy exclusionsWhat You Can Do:If your claim is delayed or denied unfairly, raise a grievance with the insurer. If unresolved, escalate to:IRDAI: https://igms.irda.gov.in Insurance Ombudsman: https://cioins.co.inFinal Thoughts: Be Prepared, Stay InformedUnderstanding the insurance claims settlement process is your first line of defence against unnecessary delays and rejections. Whether it's a health emergency, a car accident, or a family tragedy, knowing what to expect empowers you to act swiftly and confidently.Quick Tips:Read your policy terms carefully Keep documents handy and updated Don’t delay in informing your insurerFollow up regularly after filing the claimShare Your ExperienceHave you recently gone through the insurance claims settlement process in India?Share your story below—or reach out to our team if you'd like help spreading awareness and guiding others.This guide is part of our ongoing insurance literacy series. Subscribe to stay informed on policy tips, claim rights, and financial protection advice.

Continue Reading

A growing number of Indian policyholders are discovering that they may have been victims of mis-sold insurance—policies they didn’t fully understand, didn’t need, or were tricked into buying. Whether it’s life insurance, health cover, or bundled policies tied to loans or credit cards, mis-selling continues to be a widespread concern.If you suspect you were misled into buying an insurance policy, don’t panic. Here’s a practical, step-by-step guide to filing a complaint and taking back control.What Is Mis Sold Insurance?Mis sold insurance refers to any insurance policy sold under misleading, incomplete, or false information. This can include:Being sold a policy without full disclosure of terms and conditions Not being informed about exclusions, lock-ins, or waiting periods Being promised high or guaranteed returns that don't exist. Having insurance added unknowingly while taking a loan or credit card.Most cases of mis-selling in India occur through overzealous agents, third-party banking channels (bancassurance), or misleading advertisements.Step 1: Review Your Policy and Collect EvidenceBefore filing a complaint, gather all the documentation that proves your case:Original policy documents or bond Proposal form and application papersEmail or SMS communication from the insurer or agent Bank statements or premium receiptsWritten notes of any verbal promises or misleading claimsThe more details you provide, the easier it will be to prove that you were misled.Step 2: Raise a Complaint with the Insurance CompanyStart by complaining directly to the insurer’s grievance redressal cell. Here’s how: Submit a formal written complaint via their website or grievance portalEmail the grievance officer (contact details are on the insurer’s official site) Visit a branch and submit a signed complaint letterMake sure you get a written acknowledgment or complaint reference number. Under IRDAI guidelines, insurers must respond within 15 working days.Step 3: Escalate the ComplaintIf the insurer’s reply is unsatisfactory or if there is no response within 15 days, you can escalate it through two official channels:Option 1: IRDAI – Integrated Grievance Management System (IGMS)Website: https://igms.irda.gov.inToll-Free Number: 155255 or 1800 4254 732Submit your complaint and upload supporting documentsOption 2: Insurance OmbudsmanA free, region-based dispute resolution forumYou must first file a complaint with your insurer before contacting the Ombudsman Visit https://cioins.co.in to find your region’s OmbudsmanNote: The Ombudsman’s decision is binding on the insurer but not on the customer. You still retain the right to take legal action if needed.Why Is Mis Sold Insurance a Growing Problem in India?Reports from the Insurance Regulatory and Development Authority of India (IRDAI) indicate thousands of mis-selling complaints every year. Many victims are:Senior citizens lured by false promises of guaranteed returns First-time buyers unaware of policy clausesCustomers misled by digital ads or bank agentsThe pressure to meet sales targets often leads to aggressive and unethical selling practices, making consumer awareness more important than ever.Final Thoughts: Know Your Rights, Take ActionIf you think you’ve been sold the wrong insurance product, don’t stay silent. Under Indian law, you are protected. Make use of the free-look period—a window of 15 days (30 days for online/distance sales) to cancel any policy you’re unsure about.Quick Tips:Ask questions before signing anythingRead the policy document carefully—not just the brochureKeep all communication and receipts File your complaint without delayShare Your ExperienceHave you been a victim of mis sold insurance in India?Tell us your story in the comments—or contact our team to raise awareness and help others avoid the same pitfalls.This article is part of our ongoing consumer protection series. Subscribe to stay informed about your rights in finance, insurance, and more.

Continue Reading

Fraud has emerged as the most significant challenge facing the insurance industry today, according to Ramaswamy Narayanan, Chairman and Managing Director of the General Insurance Corporation of India (GIC Re). Across health, motor, and agriculture insurance, fraudulent activities are causing financial losses, eroding trust, and making insurance less accessible for genuine policyholders. In this blog, we explore why fraud is such a big problem, how it manifests, and what steps are being taken to address it.Understanding Insurance FraudInsurance fraud occurs when someone deliberately deceives an insurance company to gain financial benefits they are not entitled to. This can involve fake claims, misrepresentation, or even the creation of false policies. Fraud not only affects insurers but also leads to higher premiums and reduced trust among customers.Common Types of Insurance FraudHealth Insurance Fraud: Submitting fake medical bills, inflating treatment costs, or undergoing unnecessary procedures to claim more money.Motor Insurance Fraud: Staging accidents, inflating repair bills, or filing claims for non-existent vehicles.Agriculture Insurance Fraud: Falsifying crop loss reports or misusing government-backed schemes for personal gain.Agent and Internal Fraud: Agents or employees creating fake policies, diverting premiums, or colluding with outsiders.Why Is Fraud Such a Big Problem?Financial ImpactFraudulent claims increase the overall cost of insurance, which insurers often pass on to honest customers through higher premiums. In India, industry experts estimate that fraud accounts for 10-15% of all insurance business losses.Erosion of TrustWhen fraud becomes common, it undermines the trust between insurers and policyholders. People may become hesitant to buy insurance, fearing that claims will be unfairly rejected or that premiums will keep rising.Regulatory and Operational ChallengesThe lack of regulation in sectors like healthcare allows costs to rise unchecked, making it easier for fraud to occur. Additionally, limited reach in rural areas and reliance on agents create opportunities for mis-selling and fraudulent activities.Insights from GIC Re ChiefRamaswamy Narayanan emphasizes that fraud is a problem across all segments—health, motor, and agriculture insurance. He points out that:Health Insurance: Hospitals often increase treatment costs for insured patients, leading to higher claims and more opportunities for fraud.Motor Insurance: Many compulsory motor insurance policies are not purchased, and fraudulent claims are common.Agriculture Insurance: New schemes with poor pricing and risk coverage have made the sector vulnerable to scams, with some companies avoiding reinsurance altogether due to capped losses.Narayanan also highlights the need for better regulation, especially in healthcare, and the importance of educating people about insurance to reduce fraud.How Fraud Affects EveryoneHigher Premiums: Honest policyholders end up paying more as insurers raise premiums to cover losses from fraud.Reduced Coverage: Insurers may become stricter in settling claims, making it harder for genuine claims to be approved.Lower Penetration: As insurance becomes more expensive and less trustworthy, fewer people buy policies, especially in rural areas.Measures to Combat FraudIndustry InitiativesBima Sugam Platform: The Insurance Regulatory and Development Authority of India (IRDAI) has introduced this platform to share insurance data and detect fraud more effectively.Stronger Anti-Fraud Policies: Insurers are implementing stricter checks, regular audits, and awareness programs to prevent, detect, and report fraud.Credit Score Linkage: There are discussions about linking fraudulent claims to a person’s credit score, making it harder for repeat offenders to get away.Policyholder AwarenessAlways verify the authenticity of insurance agents and policies.Pay premiums directly through official channels to avoid premium diversion scams.Report suspicious activities or documents to the insurer immediately.How Bimacure Can HelpBimacure is dedicated to fighting insurance fraud and protecting the interests of both policyholders and insurers. By using advanced technology and data analytics, Bimacure helps identify, investigate, and deter fraudulent activities in the insurance sector. Their team works closely with clients, insurance companies, and law enforcement agencies to gather evidence, validate claims, and build strong cases against fraudsters. Bimacure also educates individuals about the consequences of fraud and promotes transparency, helping to restore trust in the insurance industry. Whether it’s recovering unclaimed insurance amounts or resolving disputes, Bimacure’s expertise ensures that genuine policyholders get the support they deserve while keeping fraudsters at bay.ConclusionFraud is the biggest problem facing the insurance industry today, affecting everyone from companies to policyholders. By understanding how fraud works and supporting industry efforts to combat it, we can help create a safer and more reliable insurance environment for all. With solutions like Bimacure leading the way, there is hope for a more transparent, fair, and trustworthy insurance sector in the future. By working together, we can ensure that insurance fulfills its promise of protection and security for all.

Continue Reading

Have you been denied a rightful insurance claim? Misled by an agent? Or discovered your policy has hidden terms that were never disclosed? If yes, it may be time to file an official insurance fraud complaint.In India, there are clear legal pathways to file grievances against insurance companies, and this guide will walk you through them—step by step.What Is an Insurance Fraud Complaint?An insurance fraud complaint refers to an official grievance lodged by a policyholder when an insurance company or its agents engage in deceptive practices, including:False assurances during policy sale denial of genuine claims without proper reason tampered policy documents or forged signatures unauthorized issuance of policies Non-disclosure of critical terms and exclusionsIf you've faced any of these, you're entitled to raise your voice through India’s regulatory framework.Step 1: File a Complaint with the Insurance CompanyAs per IRDAI (Insurance Regulatory and Development Authority of India) guidelines, your first step must be to report the issue directly to the insurer.Here's How to Do It:Lodge a complaint through the insurer’s Grievance Redressal PortalEmail the Grievance Redressal Officer (GRO) – details are listed on every insurer’s official websiteVisit the nearest branch and submit a signed written complaintKeep a copy of the acknowledgment or complaint number. As per IRDAI norms, the insurer must resolve the complaint within 15 days.Step 2: Escalate via IRDAI – IGMS PortalIf the insurer fails to respond within the timeframe or gives an unsatisfactory reply, escalate the matter by filing an insurance fraud complaint with IRDAI.Use the Integrated Grievance Management System (IGMS): https://igms.irda.gov.inToll-Free Numbers: 155255 or 1800 4254 732 Email: complaints@irdai.gov.inAttach:The original complaint reference number Policy documents and supporting evidence A clear description of the issueIRDAI will monitor the case and follow up with the insurer.Step 3: Approach the Insurance OmbudsmanIf your complaint is still unresolved or unfairly rejected, you can approach the Insurance Ombudsman—an independent authority that handles consumer insurance disputes for free.Key Details:You must have first raised the complaint with the insurerThe complaint must be filed within 1 year of the insurer’s final response The Ombudsman’s decision is binding on insurersHow to File:Visit https://cioins.co.in Locate your regional officeFile online or send a written application with all supporting documentsStep 4: Legal Action (if necessary)If the Ombudsman cannot resolve the issue, or if you're dealing with criminal fraud such as forgery or unauthorized policy issuance, you can take legal action:File a case with the Consumer ForumLodge an FIR at your local police station (in cases of fraud or identity misuse) Approach a civil court for recovery or compensation if the claim value is highReal Challenges Faced by ConsumersCommon triggers for insurance fraud complaints include:Claim denials due to hidden exclusions Fake or unauthorized policy issuancePressure sales by bank agents (bancassurance) Disputes over claim amounts in motor and health policiesThe good news: India’s legal system and insurance regulations are built to protect you—as long as you take action.Final Thoughts: Take Control of Your RightsIf you've experienced fraud, delays, or unfair treatment by an insurer, don’t stay silent. Filing an insurance fraud complaint is your right—and often the only way to get justice and prevent future misconduct.Quick Checklist:Keep all records: policy docs, emails, bills, call logs File your first complaint with the insurerEscalate via IGMS if neededApproach the Ombudsman or courts if unresolvedShare Your StoryHave you filed an insurance fraud complaint in India recently?Tell us your experience in the comments—or reach out to our team if you’d like your story to help others navigate their claims.This article is part of our Consumer Protection India series. Follow us for more on financial literacy, insurance rights, and dispute resolution.

Continue Reading

The Insurance Regulatory and Development Authority of India (IRDAI) has established panels composed of whole-time members to address violations of regulatory norms by insurers and intermediaries. This decision, made during the 132nd meeting of the IRDAI, comes amidst concerns over issues such as data leakage and mis-selling of policies within the insurance sector.These panels are part of the IRDAI's enforcement function and are tasked with deciding on observed violations of the Insurance Act and its regulations. In addition to scrutinizing regulatory breaches, the IRDAI has also formed a panel of whole-time members to review specific share transfer applications and other related matters, demonstrating a delegation of powers by the Authority.In other key decisions from the meeting:The initial application (R1 application) for Kiwi General Insurance was approved . Companies seeking registration as an Indian Insurance company must navigate three stages: R1, R2, and R3.The 'Rural, Social Sector and Motor Third Party obligations' under IRDAI regulations for the 2025-26 and 2026-27 financial years received approval .The release of the Technical Guidance Document for Second Quantitative Impact Study (QIS 2), aimed at implementing Risk Based Capital (Ind-RBC), was also approved.These actions by IRDAI reflect a broader push for enhanced vigilance in the insurance sector. The finance ministry has previously urged the IRDAI to improve oversight on claim settlements and grievance redressal, particularly in light of rising health insurance premiums and corporate governance concerns. There have been reports of health insurance premiums increasing by almost 15% in some cases this year, leading to policyholders opting out. The government has expressed its desire for these issues to be addressed urgently, potentially through new protocols before the Insurance Amendment Bill is passed.

Continue Reading

The Insurance Regulatory and Development Authority of India (IRDAI) has introduced a draft for a new rule aimed at making insurance claim complaints faster and easier to solve. The draft, called the Internal Insurance Ombudsman Guidelines 2025, was released on July 24, 2025.What’s the Big Change?Under this new rule, every insurance company that has been operating for more than three years must appoint an internal ombudsman. This person will handle customer complaints related to insurance claims up to ₹50 lakh. The goal is to solve problems inside the company quickly so customers don’t have to wait long or go to outside offices or courts.How Will It Work?Each insurance company will have at least one internal ombudsman. If needed, companies can appoint more ombudsmen for different regions to speed things up. These ombudsmen will report directly to the Managing Director (MD) or CEO for daily work, but for important matters, they will be accountable to the company’s Board or a special committee focused on protecting policyholders. This system is meant to keep the ombudsman independent and trustworthy.Why Is This Important?The new rules aim to build trust between customers and insurance companies by making complaint handling quicker and more fair. It will reduce delays in settling claims and avoid long legal battles. Insurance companies will also become more responsible for solving customer problems.Details and FeedbackThe draft includes details like the qualifications, job term, salary, and duties of the internal ombudsman. IRDAI is welcoming suggestions and feedback from the public until 5 PM on August 17, 2025. The draft can be found on IRDAI’s official website.This move is part of IRDAI’s bigger plan to protect insurance policyholders and make the system work better for everyone.

Continue Reading

Hospital Visit Turns Into an Unexpected BattleSumit Kumar, a business consultant living in Pune, was faced with every family’s nightmare: his wife had a persistent fever, and local clinics weren’t able to help. After several attempts at getting her better, he took her to Manipal Hospital on July 15. He called his health insurer, Star Health Insurance, before heading there—and was told they would approve a cashless treatment.A Doctor’s Advice, But Insurer Says "No"Since the hospital’s outpatient department was closed that day, they went straight to the emergency ward. The emergency doctor quickly started IV treatment and recommended hospitalisation, worried the symptoms might be linked to dengue or that the fever could return. Sumit’s wife was admitted for observation, staying over 48 hours in the hospital.Sumit even double-checked with Star Health. A representative assured him, “If she is admitted for more than 24 hours, your claim will be approved.” But things did not go as promised.Three Claim Rejections, No Clear ExplanationDespite following the doctor’s advice and the lengthy hospital stay, Star Health rejected the claim three times. Each time, they responded that “hospitalisation was not medically necessary.” Sumit was left confused and frustrated. “Who are they to decide that over the doctor?” he said.Trying to resolve things, he submitted three separate letters from the treating doctor explaining the need for his wife’s admission. But Star Health dismissed all the letters with generic, copy-paste explanations.Emotional Stress and Financial BurdenWhile dealing with his insurance company, Sumit also spotted a billing error at Manipal Hospital and negotiated the bill down to ₹41,000, which he paid himself for the time being. The financial impact was tough, but dealing with the repeated claim rejections made things even worse. Sumit described the experience as “emotionally exhausting.”The Turning Point: Going Public on LinkedInAfter being ignored one too many times, Sumit shared his ordeal publicly through a LinkedIn post on July 26. The post quickly got attention, racking up thousands of views and comments, including similar stories from other people. The sudden public scrutiny changed everything. The next day, Star Health called Sumit, apologised, and approved his claim—not for the full amount, but at least ₹36,000.Sumit didn’t provide any new documents; all that changed was that his complaint went viral. As he said, “We pay premiums for peace of mind, not for mental harassment.”What the Insurance Company SaidStar Health Insurance explained that their team of medical professionals reviews each claim based on medical evidence. They stated that the paperwork initially submitted didn’t prove the hospitalisation was necessary and that there were also billing discrepancies. The company claimed to have communicated with Sumit during the process and said that once a revised bill and complete case papers were given, the claim was finally processed and paid out.Final ThoughtsSumit’s story highlights how insurance claims can be an uphill battle—and sometimes, it takes public attention to get a resolution. For many, it’s a reminder that standing up and speaking out can make a difference, but it shouldn’t take going viral to be treated fairly.

Continue Reading

The Insurance Regulatory and Development Authority of India (IRDAI) has issued the draft Internal Insurance Ombudsman Guidelines, 2025, on Wednesday, July 24, 2025. Under these proposed rules, insurance companies will be required to appoint an Internal Ombudsman to handle claim-related complaints up to ₹50 lakh.Goal: Faster and Fair Complaint ResolutionThe initiative aims to establish a more independent and transparent grievance redressal mechanism within insurance companies. This move is expected to speed up the resolution of rising or pending complaints while ensuring fairness. The guidelines will be applicable to all insurers (except reinsurance companies) that have been in operation for over three years.Appointment and Role of the Ombudsman Mandatory Appointment – Every eligible insurer must appoint at least one Internal Ombudsman. Regional Requirement – Additional Ombudsmen may be appointed for different regions to ensure faster processing of complaints. Reporting Structure – Administrative matters: Reports to the MD or CEO of the company. Functional matters: Reports directly to the Board or the Policyholder Protection & Grievance Committee. This dual reporting system is designed to maintain the Ombudsman’s independence and improve oversight. By resolving disputes internally, companies can reduce the need for policyholders to approach external Ombudsman offices or courts, thus strengthening trust in the insurance sector.Key Provisions in the Draft GuidelinesThe draft specifies: Eligibility and qualifications for the Ombudsman. Tenure and remuneration details. Clearly defined duties and responsibilities. Public Feedback InvitedIRDAI has invited comments and suggestions from the public until 5:00 PM on August 17, 2025. The full draft is available on the IRDAI official website.Part of a Larger Reform PlanThese proposed guidelines are a part of IRDAI’s broader strategy to: Reduce the time taken for dispute resolution. Ensure better protection for policyholders. Enhance accountability within insurance companies. By implementing this system, IRDAI aims to make the complaints process faster, fairer, and more transparent, benefiting both policyholders and the insurance industry.

Continue Reading

Life insurance mis selling is a widespread issue that can cost you dearly, leaving you without the coverage you truly need while draining your finances. Understanding the warning signs and knowing how to safeguard yourself can help you avoid falling prey to deceptive practices. Let’s explore what life insurance mis selling looks like, the red flags to watch for, questions to ask before buying, and steps to protect yourself effectively.What Is Life Insurance Mis Selling?Life insurance mis selling happens when you are coaxed, tricked, or pressured into buying an insurance policy that doesn’t suit your needs or doesn’t deliver what you were promised. Often, people don’t realize they have been victims of life insurance mis selling until much later, typically during claims or withdrawals. Common forms of mis selling include:The Bait and Switch: You think you’re buying a simple investment like a fixed deposit, but you end up with a life insurance policy instead.Unrealistic Promises: Agents promise guaranteed high returns or loans that aren’t part of the plan.Pressure Tactics: You are rushed to sign paperwork without time to understand the policy or told offers expire immediately when they do not.Hidden Information: Important details about fees, lock-in periods, or exclusions are omitted or glossed over.Wrong Policy for Your Needs: For example, selling a long-term plan to a senior citizen who doesn’t benefit from it.Recognizing these life insurance mis selling tactics early on is crucial to avoid financial losses and inadequate protection.Red Flags That Indicate Life Insurance Mis SellingYour intuition can be an invaluable tool. If something feels off during the buying process, it likely is. Watch out for these warning signs of life insurance mis selling:Too Good to Be True Returns: If returns promised are much higher than traditional safe investments, be wary.Pressure to Sign Now: Legitimate insurance products don’t require immediate decisions.Vague or Confusing Explanations: Lack of clear communication about policy details is suspicious.Refusal to Provide Documents: If you can’t take the documents home or are discouraged from reading them carefully, be cautious.Verbal Promises Without Proof: Anything important should be clearly stated in writing, not just verbally.These red flags can help you steer clear of being misled in life insurance mis selling scenarios.Essential Questions to Ask Before Buying Life InsuranceAsking the right questions can expose life insurance mis selling attempts before you commit. Be upfront and demand clear answers to:About the Policy:Exactly what type of policy am I buying? Is it term insurance, whole life, or a combined investment plan?What benefits are guaranteed versus those that are only projected?What charges or fees will be deducted from my premiums?When and how can I access my money? Are there penalties for early withdrawal?About Returns and Benefits:Are the returns guaranteed or merely projected?If returns don’t meet projections, what happens?Can you show these details clearly in the policy document?About Your Commitment:How long am I required to pay premiums?What are the consequences if I miss a payment?Is cancellation possible? What are the costs involved?About the Company and Agent:Is the company registered with the Insurance Regulatory and Development Authority of India (IRDAI)?What is your agent license number?Where and how can I lodge complaints if issues arise?If you don’t get transparent and easy-to-understand answers to these questions, reconsider proceeding to avoid life insurance mis selling.Practical Steps to Avoid Falling Victim to Life Insurance Mis SellingProtecting yourself from life insurance mis selling involves a proactive approach:Understand Your Needs First: Know how much coverage you require and whether you want pure protection or an investment-linked policy.Shop Around: Get quotes and information from various companies to understand the market and avoid being swayed by one agent.Read Every Document Thoroughly: Never sign anything without reading and understanding it fully. Ask for explanations whenever something is unclear.Take Your Time: Don’t rush decisions. Review all documents at your leisure and involve trusted family members or advisors if needed.Verify Credentials: Confirm the company’s IRDAI registration and the legitimacy of the agent through official channels.Demand Written Proof: Any promises about returns or benefits must be documented in the policy paperwork; verbal assurances are unreliable.Following these steps greatly reduces your chances of being caught in life insurance mis selling traps.What to Do If You Suspect Life Insurance Mis SellingIf you suspect that you have been mis-sold a life insurance policy, there are ways to respond:Free Look Period: Most policies include a 15- to 30-day free look period during which you can cancel without penalty.File a Complaint: After this period, complaints can be lodged with the insurance company, the Insurance Ombudsman, or IRDAI. These bodies can help with resolving disputes and obtaining refunds or policy adjustments.Seek Professional Advice: Complex cases often require the assistance of insurance or legal experts to navigate.How We Help You Fight Life Insurance Mis SellingAt Bimacure, we witness the consequences of life insurance mis selling every day. We are dedicated to helping victims reclaim their money and get the compensation they deserve. But prevention is just as important — we empower you with knowledge and support to carefully select insurance policies that truly meet your needs.Your financial future deserves transparency and honesty. Stay vigilant, ask the right questions, and don’t let life insurance mis selling put your security at risk.By understanding life insurance mis selling, recognizing warning signs, asking critical questions, and following careful steps, you can safeguard your investments and peace of mind. Be informed, be patient, and take control of your insurance journey.

Continue Reading

Getting older should never mean compromising on quality healthcare coverage. If you're a senior citizen worried about finding affordable insurance or facing claim rejections due to your age or health conditions, recent guidelines from the Insurance Regulatory and Development Authority of India (IRDAI) bring promising changes designed for you. These updates remove age barriers, protect your rights, and offer enhanced benefits to ensure your healthcare needs are effectively met throughout your golden years.No Age Limits for Health InsuranceEarlier, the maximum age to purchase health insurance was often capped at 65 years, leaving many seniors without options after this age. The IRDAI has completely removed this upper entry age limit. Now, seniors aged 70, 75, or even 80 can buy new health insurance plans without restriction. This revolutionary change acknowledges that health issues often increase with age and ensures seniors have the freedom to secure coverage whenever they need it, providing peace of mind and financial security against medical expenses.Free Health Coverage for Seniors Above 70A major step forward for senior citizens is the expansion of the Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB-PMJAY). Effective from September 2024, all senior citizens aged 70 and above can avail free health insurance coverage regardless of their income status. This scheme offers coverage up to ₹5 lakh per family annually, covering surgeries and complex procedures. The universal inclusion under this scheme benefits approximately 6 crore elderly individuals nationwide, making essential healthcare accessible without financial worries.Protection Against Health Condition-Based Claim RejectionsOne of the biggest fears for senior citizens has been claim rejection due to pre-existing or chronic health conditions like cancer, heart disease, renal failure, or AIDS. IRDAI’s new guidelines prohibit insurers from rejecting claims solely based on such severe medical conditions. This crucial protection removes discrimination and encourages seniors to confidently purchase insurance knowing their healthcare needs will be supported without unjust denials.Reduced Waiting Periods for Pre-Existing DiseasesPreviously, insurers often imposed a waiting period of up to four years before covering pre-existing diseases such as diabetes, hypertension, and joint ailments common among seniors. The new IRDAI rule reduces this waiting period to three years, allowing earlier access to benefits and faster financial relief for treatments. Additionally, waiting periods for specific procedures like knee replacement and varicose vein treatments have also been shortened to three years.Enhanced Support and Tailored Insurance ProductsTo better serve seniors, IRDAI mandates insurance companies to provide dedicated support channels with trained representatives knowledgeable about senior citizens' unique healthcare needs. This includes special helplines and customer care teams ensuring streamlined assistance during claims and queries. Furthermore, insurers are encouraged to create customized insurance products designed specifically for seniors, moving away from generic plans suited only for younger populations.Expanded Coverage and BenefitsSeniors who prefer alternative healing practices like Ayurveda, Yoga, Naturopathy, Siddha, Unani, or Homeopathy (AYUSH) have reason to celebrate. The IRDAI has lifted limits on AYUSH treatments, enabling these to be claimed up to the full insured sum. Moreover, policyholders are now allowed to file multiple claims across different insurers if holding benefit-based policies, adding flexibility in managing complex health treatments that may involve various providers.Shortened Moratorium Period and Premium ProtectionThe moratorium period—the time after which insurers cannot reject claims except in cases of fraud—has been reduced from eight years to five years. This means after continuously renewing a policy for five years, seniors gain greater claim security. Additionally, IRDAI restricts annual health insurance premium hikes for senior citizens to no more than 10% without prior approval, helping keep health insurance affordable in the long term.Your Rights as a Senior Citizen PolicyholderThe IRDAI has also formalized important rights to protect senior policyholders:Insurance companies must provide written reasons if your application or claim is rejected.You have the option to change your Third Party Administrator (TPA) where feasible.At least 50% of your pre-insurance medical examination costs must be reimbursed once your policy is accepted.Insurers cannot refuse policy renewal except in cases involving fraud, moral hazard, or misrepresentation.How Bimacure Supports YouEven with these positive guidelines, navigating the insurance landscape can be complex. Bimacure offers expert help to seniors facing claim rejection, policy disputes, or any challenges in obtaining rightful benefits. Their experienced team provides guidance on your rights, helps file complaints against insurers not complying with IRDAI rules, and supports you through claim disputes.Moving Forward with ConfidenceThe IRDAI's new health insurance guidelines mark a significant stride in making healthcare accessible and affordable for senior citizens. Age or health conditions are no longer barriers to quality coverage. Seniors can now enjoy dedicated support, shorter waiting times, free coverage options, and enhanced policy benefits for comprehensive protection. If there are any issues with your health insurance or claim, reaching out for expert assistance can ensure these regulatory changes translate to real advantages for your health and peace of mind.Frequently Asked QuestionsWhat are the new IRDAI guidelines for senior citizen health insurance?They include removing the 65-year entry age limit, providing coverage under Ayushman Bharat for seniors above 70 regardless of income, reducing waiting periods from 4 to 3 years for pre-existing conditions, prohibiting claim rejection based on severe medical conditions, and mandating dedicated support channels.Can I buy health insurance after the age of 65?Yes, seniors at any age above 65, even up to 80 years, can purchase new health insurance policies without any maximum age restriction.What does free health coverage above 70 years mean under IRDAI rules?Seniors aged 70 and above are eligible for free health insurance under the Ayushman Bharat Pradhan Mantri Jan Arogya Yojana, which provides coverage of ₹5 lakh per family per year.Has the waiting period for pre-existing diseases reduced?Yes, the waiting period for coverage of pre-existing conditions like diabetes, hypertension, and surgeries like knee replacement has been reduced from 4 years to 3 years.These changes empower senior citizens to access quality healthcare insurance easily, ensuring their health needs are met affordably and without discrimination.

Continue Reading

In an unprecedented move, the Insurance Regulatory and Development Authority of India (IRDAI) has suspended one of its own junior officials, B.H. Suryanarayana Sastry, an assistant manager, on charges of financial misconduct. The suspension order, issued on August 21, 2025, and signed by Rajay K. Sinha, Member, Distribution, IRDAI, is a significant development in the typically reserved regulatory body.The Allegations: A Tale of Embezzlement and ManipulationWhile the IRDAI's suspension order states that Sastry has admitted to his wrongdoing, it doesn't specify the exact nature of the misconduct. According to sources, the charges against Sastry are severe, alleging fund embezzlement and the siphoning of crores of rupees from the regulator's coffers. A complaint filed with the Economic Offences Wing (EOW) of the Cyberabad police sheds more light on the matter. The complaint alleges that Sastry, whose role involved processing vendor payments, manipulated invoices and diverted an estimated Rs 5.3 crore into multiple personal bank accounts over a nine-month period. An internal audit reportedly flagged unusually high payouts cleared by Sastry, leading to the discovery of fraudulent transactions.Questions Arise in the Wake of the SuspensionThis incident, a first of its kind for IRDAI, has raised a number of questions within the financial community and among the public. The lack of specific details in the official suspension order has sparked curiosity and concern. While the suspension demonstrates a commitment to internal accountability, the full extent of the misconduct and how it went undetected for months remains to be seen. The police investigation is now underway to track the trail of the embezzled funds and determine if others were involved.This case serves as a stark reminder that even regulatory bodies, tasked with maintaining the integrity of the financial system, are not immune to internal fraud and require robust checks and balances to prevent such incidents.

Continue Reading

Your Money, Your Future - Now Cheaper!Hey everyone, get ready for some game-changing news that's going to put more money back in your pocket and supercharge your financial security! The 56th GST Council meeting just dropped a massive bomb of good news for every Indian – and it's especially sweet for your health and life insurance!Forget the fireworks for Diwali, because the real "Diwali bonanza" is this: NO GST on individual health and life insurance policies starting September 22, 2025! 🎉That's right, you heard it correctly. From an 18% burden to absolutely ZERO PERCENT!The Big Reveal: What's Changing & How It Affects YOU!For far too long, that 18% GST on insurance premiums felt like an extra tax on securing your future. It made essential protection feel like a luxury. But not anymore!Here’s the breakdown of what becomes 0% GST:Health Insurance: This includes your individual policies, family floater plans, and senior citizen policies.Life Insurance: From crucial term life and endowment plans to your investment-linked ULIPs.What does this mean in plain English?If you renew or buy any of these policies on or after September 22, 2025, you could see your premium drop by almost 18% immediately! Imagine that – saving nearly one-fifth of your insurance cost, just like that! This isn't just a tax cut; it's a monumental step towards making vital financial and health protection accessible to every single one of us.Why This Is HUGE for India (And YOU!)India has always struggled with low insurance penetration. A big reason? The cost. The government's bold move to make insurance GST-free is a direct shot at fulfilling the vision of "Insurance for All by 2047."This isn't just about saving money; it's about:IGNITING DEMAND: Lower prices mean more people can finally afford the insurance they've always needed. Get ready for a surge in health and term plan purchases!CLOSING THE PROTECTION GAP: More families will now have a crucial safety net against life's unpredictable challenges, from medical emergencies to unforeseen losses.BOOSTING THE ECONOMY: While insurers will adapt, the long-term benefit of a financially secure population and a booming insurance sector is undeniable.Your To-Do List: Get Ready to Save Big!This is where you come in! Don't just read about it; act on it and reap the rewards!MARK YOUR CALENDAR (Sept 22, 2025): If your health or life insurance policy is up for renewal around this date or later, get ready for a significant premium reduction. Double-check your renewal notice for the updated, lower amount!CONSIDER YOUR OPTIONS NOW: Have you been putting off getting a new health or life insurance policy because of the cost? Now is the absolute best time to explore your options. You can get the same, or even better, coverage at a substantially lower price point.STAY ALERT FOR NEW DEALS: With the GST burden lifted, insurers might introduce new, more attractive policies or enhanced features. Keep an eye out for these opportunities to maximize your benefits.This isn't just a policy change; it's a financial revolution for the common Indian. The government has cleared the path for a more secure and healthier future for all.Don't miss out on these savings! Share this incredible news with everyone you know! Your family, friends, and colleagues deserve to know about this game-changing "Diwali Bonanza"!

Continue Reading

When Health Insurance DisappointsMany people buy health insurance expecting support during medical emergencies. But often, policyholders face frustration when their claims are rejected or only partially paid, leaving them with a financial burden. This issue is so common that many customers file complaints with the Insurance Ombudsman.Top Health Insurers Facing the Most ComplaintsAccording to the latest report from the Council of Insurance Ombudsman (CIO) for the financial year 2023-24, certain health insurance companies received the highest number of complaints from customers. The insurer with the most complaints was Star Health & Allied Insurance, which alone had over 13,000 complaints. Out of these, more than 10,000 complaints were about rejected or partially rejected claims.Following Star Health, CARE Health Insurance had around 3,700 complaints, while Niva Bupa Health Insurance recorded over 2,500. Only two public sector companies – National Insurance Co. Ltd and The New India Assurance Co. Ltd – made it to the top five.Why Does Star Health Have So Many Complaints?Star Health explains that nearly 90% of its business is from individual customers, unlike others who have many group policies. This means Star Health deals with many more personal claims, which naturally leads to more customer feedback and complaints.Complaints Per Lakh Policyholders: Fairer ComparisonTo fairly compare insurers, we can look at complaints per one lakh policyholders. This measure shows how many complaints come in relative to the size of the insurer's customer base. Here, Star Health still leads with 63 complaints per lakh policyholders, followed by Niva Bupa with 17, and CARE with 16 complaints per lakh policyholders.Main Reasons for Complaints: Claim Rejections Top the ListMost complaints are about claim denials or partial payments. Under Rule 13(1)(b) of the Insurance Ombudsman Rules, 2017, the Ombudsman can intervene specifically on such claim rejections.Star Health again leads with over 10,000 claim denial complaints taken to the Ombudsman, while CARE Health Insurance had about 2,400 such complaints.Public vs. Private Insurers: Who Gets More Complaints?Private insurers received many more complaints than public insurers. The Ombudsman got around 26,000 complaints against private health insurers, compared to just over 5,200 against public sector companies in FY 2023-24.While complaints for life and general insurance decreased compared to the previous year, health insurance complaints increased by almost 22%.New IRDAI Rules for Internal Insurance OmbudsmanTo address claim delays and rejections, the Insurance Regulatory and Development Authority of India (IRDAI) has introduced a new Internal Ombudsman system. Each insurer must now have an Internal Ombudsman to handle complaints up to Rs 50 lakhs.This Internal Ombudsman will review complaints not resolved within 30 days or partially/wholly rejected claims appealed by the policyholder. This aims to resolve issues faster inside the insurance company before escalating them externally.However, some concerns remain about whether this internal system will be fully independent, since the Internal Ombudsman reports to the insurer’s senior management.What This Means for PolicyholdersThe rise in complaints, especially against private health insurers like Star Health, highlights the challenges policyholders face in getting their claims settled. The new IRDAI Internal Ombudsman could improve the situation if implemented well, by offering faster internal resolution.Policyholders should stay informed about their rights, understand their policies clearly, and persist in following up on claim issues, using both the internal and external Ombudsman systems if needed.

Continue Reading

Insurance is meant to give us peace of mind. Unfortunately, scams in the sector are on the rise, and fraudsters are finding new ways to cheat policyholders. If you’ve ever faced claim delays, unfair rejections, or suspected foul play in your policy, you’re not alone. At Bimacure, we work every day with people like you—helping them fight back and recover what’s rightfully theirs.Common Insurance Frauds Happening Today🔹 Digital Identity Fraud: Fraudsters use fake or manipulated Aadhaar and other digital IDs to buy policies or file bogus claims. In many cases, they even change your registered mobile or email to keep you from receiving alerts.🔹 Fake Policy Scams: Fraud agents pose as genuine advisors and sell policies that look authentic but carry no real value. Victims often discover the truth only when their claims are rejected.🔹 Mis-selling: Dishonest agents promise low premiums, guaranteed returns, or unrealistic benefits. The hidden exclusions, waiting periods, and surrender charges come to light only when it’s too late.🔹 Forged Documents: From fake medical reports to falsified police documents, scammers are using forged paperwork to make false claims, especially in health and life insurance.🔹 Overbilling: Some hospitals and garages inflate bills for unnecessary or even non-existent services, leading to heavy financial losses.🔹 Staged Accidents: Motor insurance scams often involve staged or fake accidents to claim money for damages or injuries.🔹 Fake Recovery Calls: One of the latest tricks—fraudsters impersonate IRDAI or Ombudsman officials. They claim they can recover your “stuck” or “staged” claims but insist you buy new policies first. This trap keeps victims stuck in a cycle of fraud.Why You Need Bimacure’s Legal ExpertsAt Bimacure Legal Consulting, we don’t sell insurance—we protect people from fraud, mis-selling, and unfair practices. Here’s how we can help:✔ Fraud Detection: Our experts analyze your policies and claims, spotting red flags or manipulated documents.✔ Claim Rejection Support: We prepare strong legal responses to challenge wrongful rejections.✔ Accountability: If you’ve been mis-sold or tricked into fake policies, we help you file complaints and take action against fraudulent intermediaries.✔ Legal Guidance: We guide you through filing with IRDAI, the Insurance Ombudsman, or even Consumer Court—ensuring every step is done right.✔ Empowerment: We equip you with knowledge to avoid future scams and protect your rights.How to File a Complaint with Bimacure’s HelpIf you suspect fraud or have faced claim issues, here’s how to take action with Bimacure by your side:Collect Your Documents: Keep your policy papers, claim forms, and any communication with agents or insurers ready.Contact Bimacure: Visit our Contact Page to share your issue.Expert Review: Our legal team reviews your case and identifies whether it’s fraud, mis-selling, or wrongful rejection.File the Complaint: With our help, you can file a complaint to IRDAI, Ombudsman, or Consumer Court effectively and without errors.Stay Protected: We guide you throughout the process and also help you secure your future policies against such risks.Take the First Step TodayDon’t let fraudsters or even insurers take advantage of you. With Bimacure’s Insurance Fraud Support, you’re never alone in the fight.📞 Need immediate help? Reach us at our Contact Page or call us directly at +91 91474 13241Bimacure – Your Legal Partner in Insurance Disputes.Disclaimer: Bimacure is an independent legal consulting firm and is not associated with IRDAI or the Insurance Ombudsman in any manner.

Continue Reading