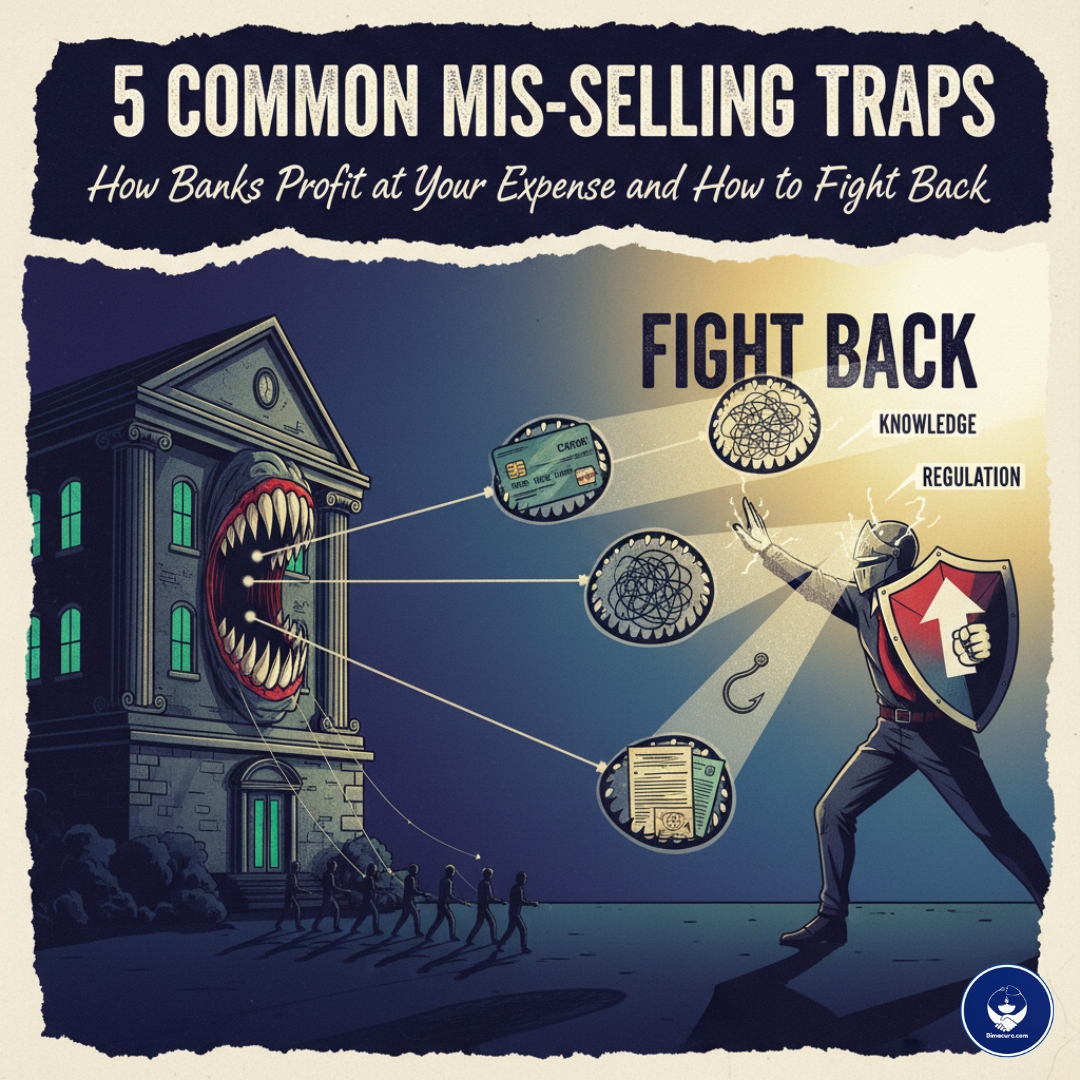

Many people trust banks and financial agents to help grow and protect their money. Unfortunately, some banks and agents may sell financial products that do not suit the customer just to earn commissions. This practice, called “mis-selling,” continues to affect countless people in India. Here’s how these traps work, and what steps can be taken to stay protected. Mis-selling isn’t an abstract problem—it happens to real people every day. For example, Rajeev bought an insurance policy based on his friend’s advice. He paid Rs. 35,000 every year but got only Rs. 8 lakh in life cover, which was not enough for his family. When he checked the surrender value later, the returns were far less than the money he put in. He realized he was led to buy a product that mostly benefited the agent through commissions, offering very low returns to him. Another case involved Gaurav, who ended up purchasing a health policy that was actually just a discount plan and not real insurance. Even after realizing the mistake, he couldn’t cancel and get his money back. These stories show how easy it is to get caught in mis-selling traps if one isn’t careful. Banks and agents are often pressured to sell more products that benefit their company rather than the customer. For relationship managers, hitting sales targets and earning rewards can become more important than matching the right product to the customer’s needs. Agents may sell high-commission plans instead of simple and effective ones like term insurance because they stand to earn more. Bank managers sometimes hide important product details, exaggerate returns, or tie up financial products with unrelated services like loans or lockers. Here are the typical tricks used to mis-sell financial products: Hiding important information like hidden costs, risks, or how commissions affect your returns. Promising “guaranteed” high returns, especially on market-linked products, when no such guarantee exists. Bundling other services (like a loan or locker) with the forced purchase of an insurance policy. Suggesting risky or unsuitable products, especially to people who need security, like senior citizens. Using discounts, freebies, or cashback offers that either don’t exist or hide the real costs. These tactics work because customers often trust the seller completely, or don’t read documents carefully before signing. Research shows that even many bank managers don’t fully understand the products they sell. Most are unable to explain key differences between several financial products. This big knowledge gap means customers are even more at risk of making poor decisions, as the person guiding them might not know enough themselves. To protect yourself: Always ask questions and never sign up for a product on the spot. Do not rely only on verbal promises; read the terms and check official documents. Be skeptical of products tied with “special offers,” cashback, or “guaranteed” returns. Demand to see all charges, terms, and potential risks written in simple terms. Preserve all records like emails, call recordings, payment receipts, and messages. If you suspect mis-selling, file a written complaint with the institution first. If unresolved, take your case to the right regulator: RBI for banks, IRDAI for insurance, or SEBI for mutual funds. Quick action is key as older complaints may not be accepted. Regulators have begun tightening rules, issuing advisories and fines, but enforcement needs to be stronger. Easy-to-understand documents showing risks, costs, and returns should be mandatory before selling any financial product. Also, changing how agents and managers are paid—so they don’t earn mostly from commissions—would reduce the motivation to mis-sell. Bank employees and agents should put the customer’s best interests first, but that doesn’t always happen. Being alert, asking the right questions, and keeping proper evidence can help individuals protect themselves from mis-selling. Remember, if something sounds too good to be true, it probably isn’t true. Stay aware and make informed decisions to keep your money safe. 📞 Need immediate help? Reach us at our Contact Page or call us directly at +91 91474 13241 Bimacure – Your Legal Partner in Insurance Disputes.Introduction

Real-Life Examples of Mis-Selling

Why Mis-Selling Happens

Most Common Mis-Selling Tactics

The Bigger Problem: Lack of Awareness

Fighting Mis-Selling: What You Can Do

How Regulations Can Improve Protection

Conclusion

We specialize in providing independent grievance redressal legal services. We are not an insurance company, broker, or intermediary registered with the IRDAI. We assist clients with insurance policy complaints by handling all documentation, communication, and legal support.

Corporate office : Merlin Infinite DN-51, Suit-603 Street No 11, DN Block, Sec V, Bidhannagar, Kolkata, WB 700091

Registered Office : 2A, Ganesh Chandra Avenue, Commerce House, 7th Floor, Room - 6A, Kolkata -70001

Bimacure.com is not related to IRDA/Ombudsman in any manner.© 2025 Copyrights by INSUCURE Solutions India (OPC) Pvt. Ltd. All Rights Reserved

ISO - 9001:2015 | ISO/IEC 27001:2022 | CIN - U70200WB2024OPC271472

Design & Develop by Webina Tech